About Me

I am currently pursuing a Master’s in Finance at Tsinghua University, after earning my Bachelor’s in Engineering from Shanghai Jiao Tong University. My undergraduate studies spanned computer vision, NLP, and time series analysis, which now influence my work in quantitative modeling and factor discovery using deep learning.

I am open to opportunities in Quantitative Research and welcome connections for collaboration or discussion. Feel free to reach out via WeChat (yins156) or email at yinelon@gmail.com. For more details, you can download my bilingual resume here.

Education

Tsinghua University, School of Economics and Management

Tsinghua University, School of Economics and Management

Master of Finance

Beijing • Sept 2025 - Jun 2027

Current Courses: Large Language Models and Generative AI, Financial Derivatives, Financial Data Analysis, Introduction to FinTech

Shanghai Jiao Tong University, School of Biomedical Engineering

Shanghai Jiao Tong University, School of Biomedical Engineering

Bachelor of Engineering (Electronic & Computer Eng. Track)

Shanghai • Sept 2021 - Jun 2025

Awards: Outstanding Graduate, Merit Student Award, First Class Academic Scholarship

Core Courses: Data Structure (A), Methods in Mathematical Physics (A), Biostatistics (A-), Medical Robot Control (A)

Teaching Assistant:  NYU Shanghai - Recommender Systems(CSCI-SHU 381), Machine Learning(CSCI-SHU 360)

NYU Shanghai - Recommender Systems(CSCI-SHU 381), Machine Learning(CSCI-SHU 360)

Internship Experience

Minghong Investment

Minghong Investment

Quantitative Research Intern

Shanghai • Dec 2025 - Present

Crypto HFT

Conducted research on crypto machine learning, market-making and arbitrage strategies in the overseas HFT prop trading team

-

End-to-End Return Forecasting Pipeline: Developed an end-to-end return forecasting pipeline for highly liquid crypto perpetual futures by converting L2 order book data into time-series inputs; leveraged multi-scale convolutional feature extraction and a regression head for prediction

-

Model Architecture Optimization: Optimized the model architecture to improve training stability and inference efficiency; extended to a multi-task setup and used attention to propagate short-term signals into longer-horizon forecasts, supporting real-time monitoring for market-making

Lingjun Investment

Lingjun Investment

Quantitative Research Intern

Beijing • Aug 2025 - Nov 2025

Stock Team

Worked primarily on model research and strategy development for A-share equities in the stock team

-

Machine Learning Cross-Sectional Forecasting: Leveraged a 1,000+ alpha-factor library for China A-share equities; built tree-based and deep learning models with rolling training around key trading dates, and delivered >10% improvement over the baseline. The best model achieved 40%+ annualized long-only return in backtests and was deployed to live trading

-

Deep Learning Time-Series Strategies: Built end-to-end time-series pipelines, implemented multiple baselines and a stacking ensemble; focused on architecture optimization, loss function design, and attention mechanisms, with hyperparameter tuning and model combination achieving 50%+ annualized return in backtests. Several baseline models were deployed to live trading

Ant Group (Alipay)

Ant Group (Alipay)

LLM Algorithm Intern

Shanghai • Apr 2025 - Aug 2025

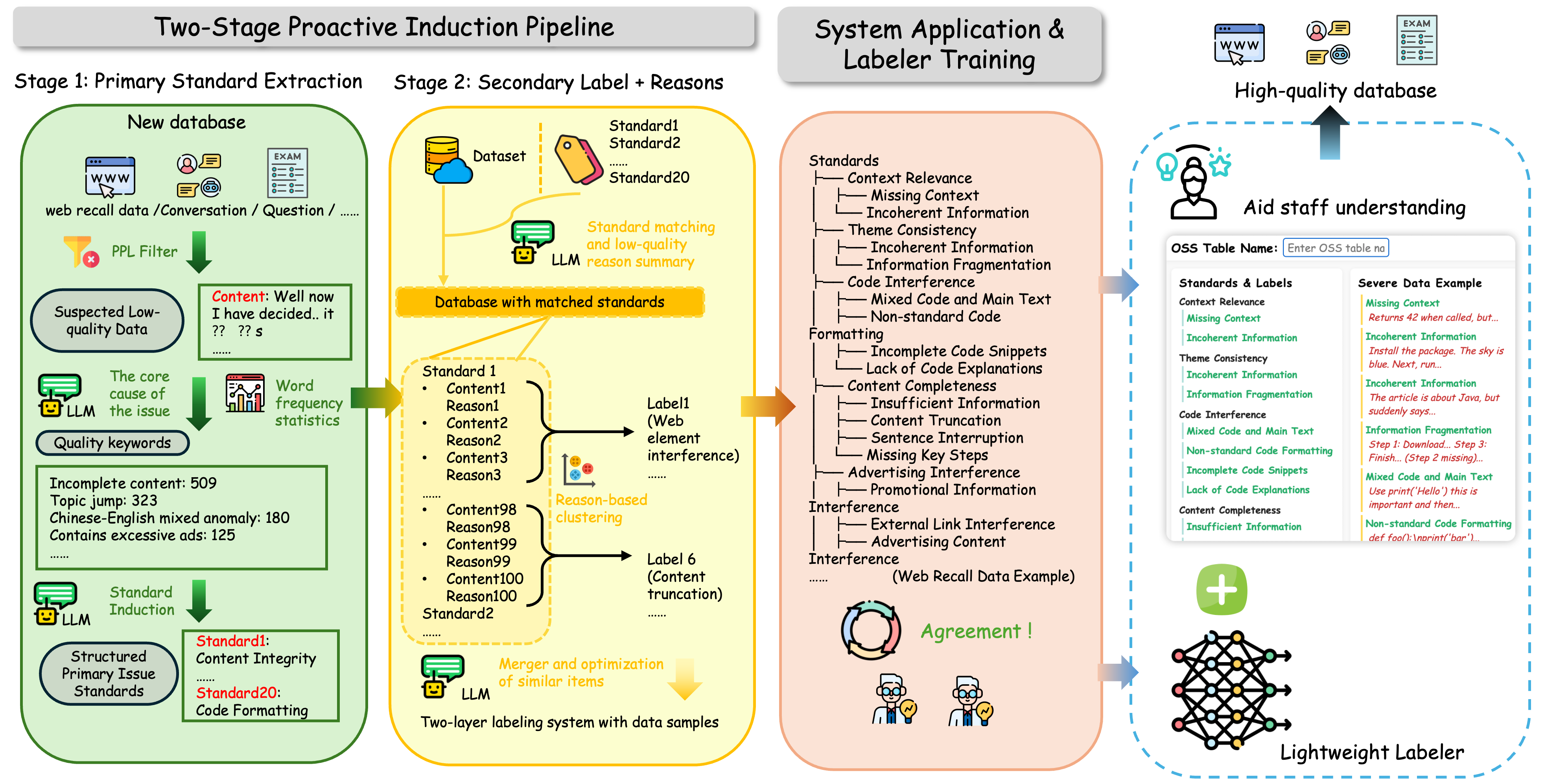

Engineered ProQ model for automated data screening on Ling LLM; fine-tuned quality-filtering LLMs and streamlined the pipeline

- Data Screening Model: Built a custom agent-based data screening and harmonization model (ProQ), pre-screening data using metrics like PPL and iteratively selecting representative data for fine-tuning quality-filtering models. Post-trained Ling MOE Lite on ~3M optimized data, improving language understanding and code completion by over 1%

- Signal-Based Data Filters: Developed rule- and model-based operators to identify low-quality data using targeted signals

Panoramic Hills Capital (AUM $4B Hedge Fund)

Panoramic Hills Capital (AUM $4B Hedge Fund)

Crypto Research Intern

Shanghai • Jan 2025 - Mar 2025

Conducted crypto market monitoring and developed sentiment indices on crypto, providing insights for fund positioning

- NLP Sentiment Index Modeling: Engineered quantitative sentiment indicator; curated datasets from X/Crypto News, LoRA-fine-tuned FinBERT on 8k labeled samples (cross-entropy loss, F1=0.91), yielding normalized daily scores [-1,1] to guide BTC trading

- Crypto Analysis: Monitored daily crypto trends; constructed financial models for BTC miners (MARA, CLSK, RIOT, etc.)

Research & Publications

Jun 2025 - Sept 2025, ICASSP 2026 In Submission

Authors: Shuo Yin, Jiahong Zhu, Tianlong Yang, Yuqiao Liu

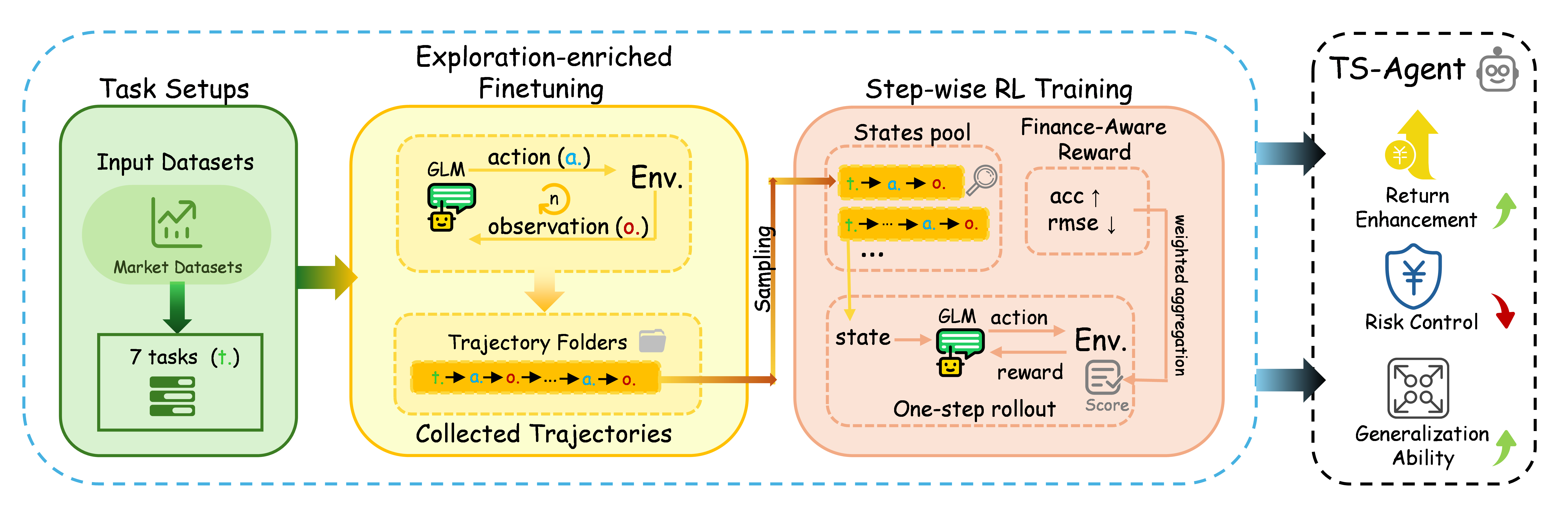

Developed TS-Agent, a reinforcement learning–based agent for financial time-series forecasting, using LLM-generated strategy pool for exploration-enhanced fine-tuning, then seeding stepwise RL from selected strategies with custom RL module.

Sep 2025 - Present, ACL 2026 In Submission

Authors: Zhaolu Kang, Junhao Gong, Wenqing Hu, Shuo Yin, Zhicheng Fang, Yingjie He, Rong Fu, Eric Hanchen Jiang, Leqi Zheng, Xi Yang, Xiaoyou Chen, Richeng Xuan

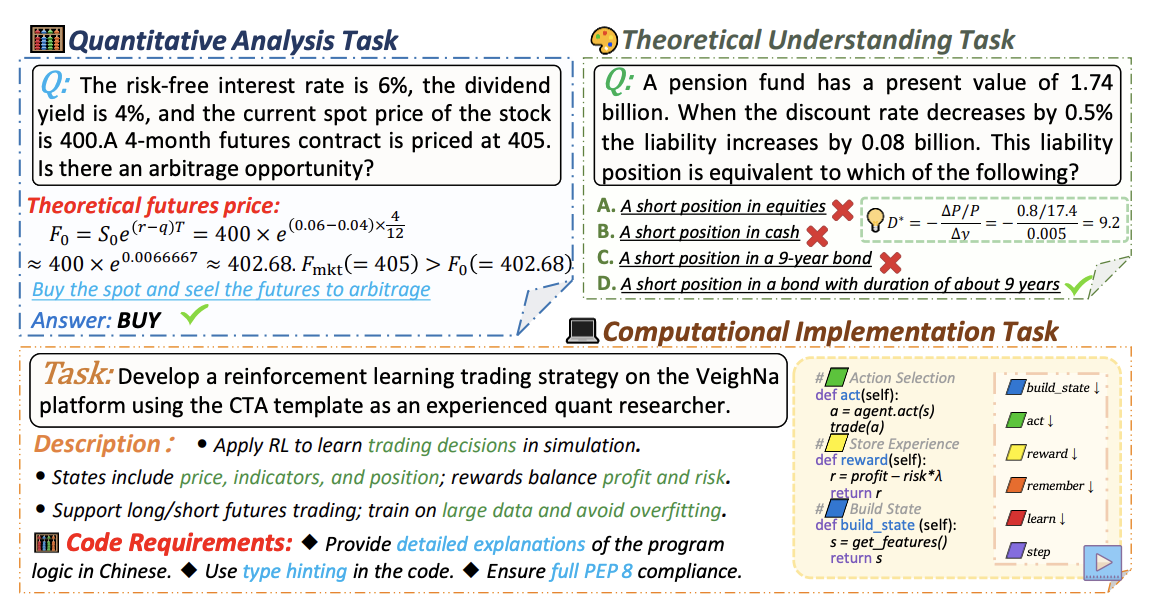

QuantEval is a new benchmark designed to evaluate Large Language Models (LLMs) in financial quantitative tasks. It assesses three areas: knowledge-based question answering, quantitative reasoning, and quantitative strategy coding. Tests on many top LLMs show major performance gaps. To address this, we apply supervised fine-tuning and reinforcement learning to improve results.

Aug 2025 - Present, KBS In Submission

Integrated Agents, Genetic Algorithms, and Flow Networks to produce diversified alpha factors Developed factor alignment and filtering framework for A-shares and cryptocurrencies, implementing data cleansing, dual-chain dynamic iteration, and agent-based reporting

Aug 2025 - Present, CVPR 2026 In Submission

Authors: Rong Fu, Chunlei Meng, Shuo Yin, Zijian Zhang, Weizhi Tang, Shaobo Wang, Youjin Wang, Simon James Fong

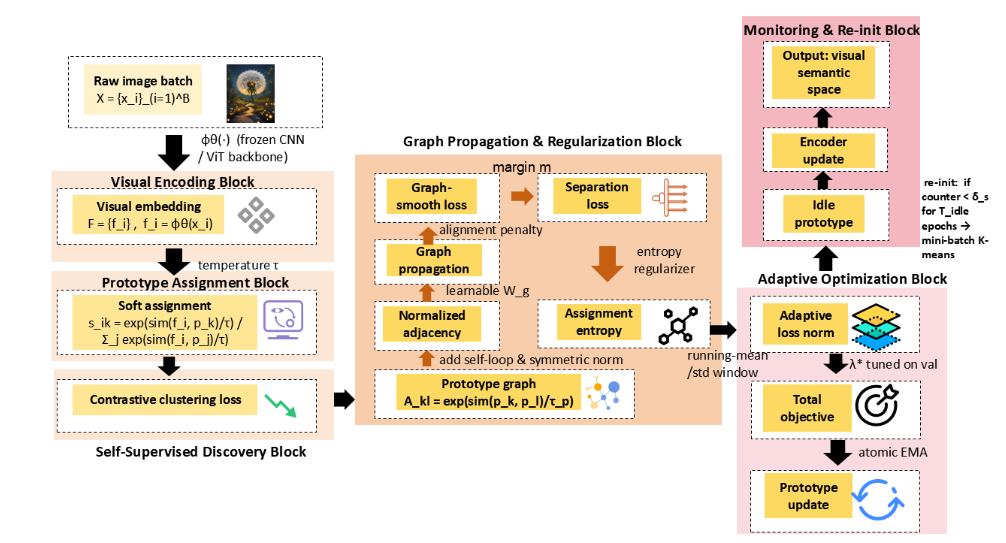

This research presents a vision-based approach that abandons text and allows visual features to communicate through a graph of image prototypes. Using self-supervised learning, the model uncovers emergent semantic structures, where meaning is determined purely by vision. Text is only used for interpretation, not during training. This method demonstrates that vision alone can recognize and name the world without relying on textual input.

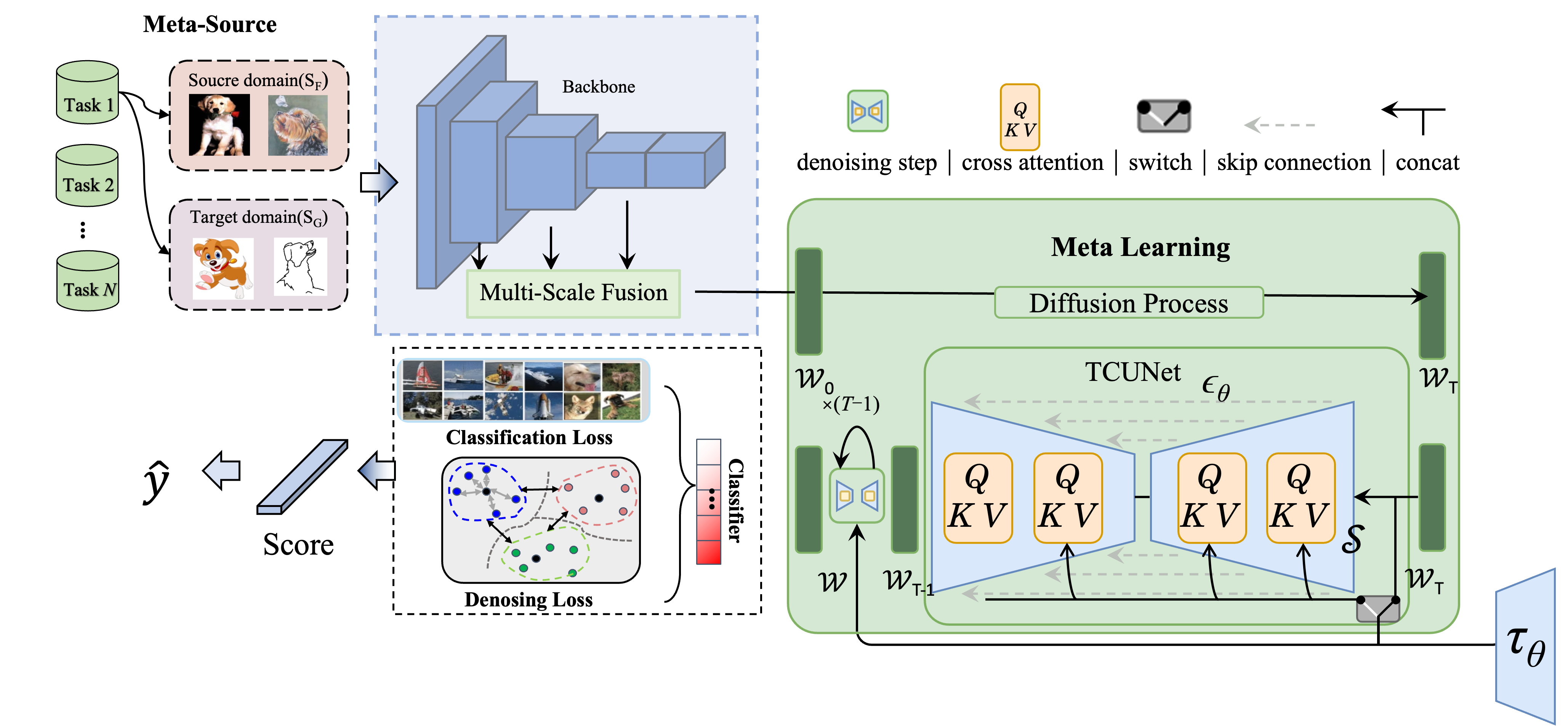

Revolutionizing Open Set Domain Generalization: Learning to generalize via Conditional Diffusion Without Gradient

PaperJul 2025 - Present, CVPR 2026 In Submission

Authors: Haidong Kang, Shuo Yin, Huiquan Zhang

This work introduces OGDiff, a novel OSDG framework that replaces expensive second-order meta-learning with a conditional diffusion process. This avoids inner-loop backpropagation, reducing computational costs and improving stability. The MSDFF module is also introduced to better capture both fine- and coarse-grained features, enhancing recognition of known and unknown classes.

Feb 2024 - Sept 2024, Published in Nonlinear Dynamics (SCI Q2)

Authors: Feier Chen, Shuo Yin, Jiahang Zhang, Yi Sha & Huaxiao Ji

Based on MF-DFA and multi-peak analysis, the multifractality of LNG spot freight rates was verified, and factor signals were established, including spectral decomposition components, peak positions, and long-range correlation strength. Using methods such as LSTM, LNG futures return predictions were made, incorporating indicators like the Hurst exponent to achieve strategy switching and window smoothing. The backtest results showed an annualized return rate exceeding 36%.

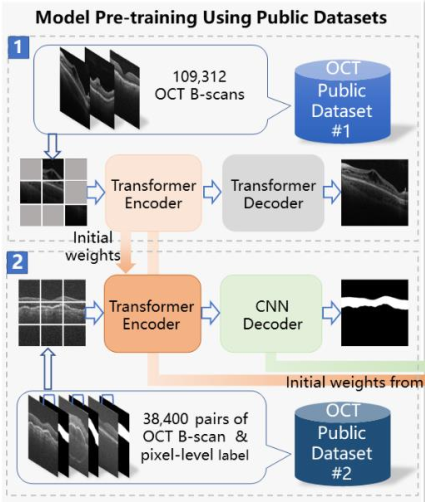

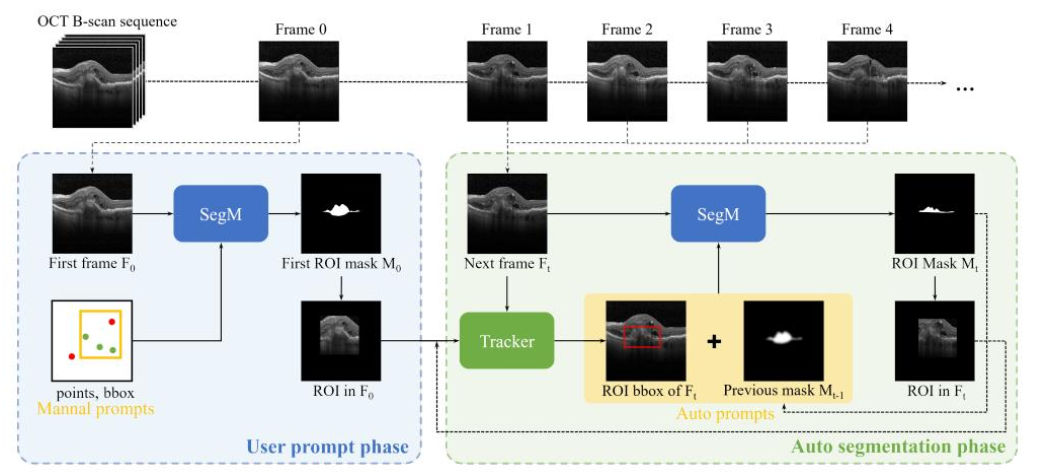

Sep 2023 - Feb 2024, Published in SPIE

Authors: Kaixiang Zhang, Haoran Zhang, Qi Lan, Zesen Chen, Shuo Yin, Yongqi Wei, Zehao Wang, Jianlong Yang

This research presents a zero-shot OCT segmentation method that overcomes the limitations of traditional deep learning approaches, which require re-labeling and retraining for unseen Regions of Interest (ROIs). The method only needs box or point prompts for ROIs in the first frame, enabling automatic segmentation in subsequent frames.

Sep 2023 - Mar 2024, Bronze Medalist

- Derived high-frequency market microstructure factors from order book and auction data, including buy-sell imbalance ratios, price-volume triple barriers, reference price lags/differentials, statistical moments, depth-weighted spreads, and volatility proxies

- Built LightGBM model with rolling training and Optuna-based hyperparameter optimization; achieved MAE of 5.473 on validation set

Jul 2022 - Feb 2023, SJTU Outstanding PRP Project

Built a real-time database by web scraping public opinions and disclosure information from trading platforms using proxy pools to enhance crawler efficiency. Fine-tuned BERT NLP model to establish a text sentiment prediction framework, providing ESG ratings for 3,000+ listed companies based on mainstream ESG rating indicators

Additional Information

Language

- English: TOEFL 108

- Chinese: Native Speaker

Interests

- Go (Weiqi): I have been a player of Go since childhood. AlphaGo is one of my motivations to study AI.

- Games: Fan of strategic games including Texas Hold’em poker, Avalon (board game), and Balatro.

- Sports: Enjoy various sports, play basketball and work out daily, currently learning tennis. Always happy to connect with workout buddies or sports partners! :)